January 2026 Market Wrap

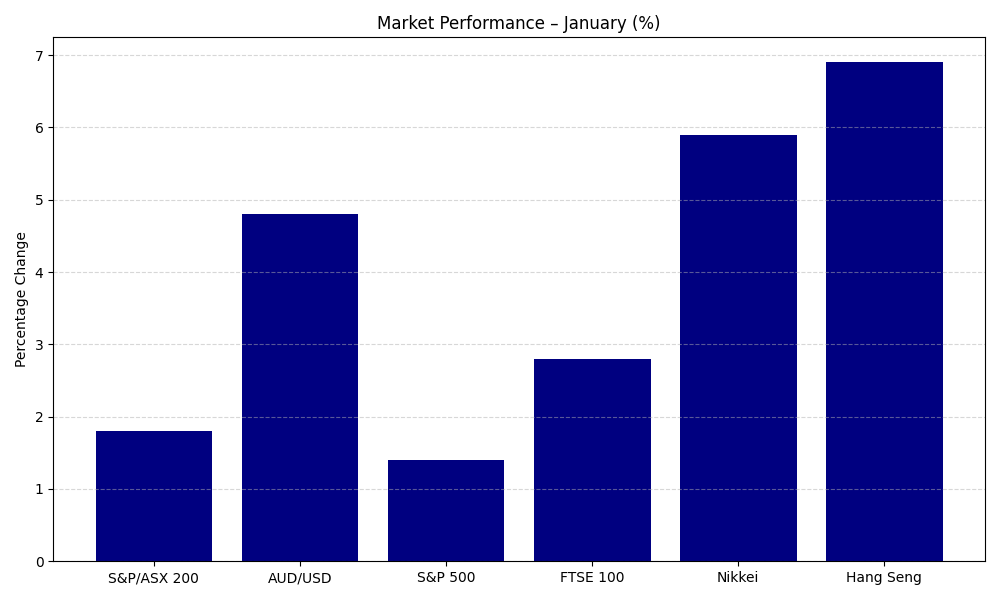

The Australian share market rose in January, with the S&P/ASX 200 Index gaining 1.8% to close at 8,869.1 points. The Australian dollar strengthened by 4.8%, now trading at 70 US cents. Although the Reserve Bank of Australia (RBA) did not meet during the month, all focus is now on whether it will keep the Cash Rate at 3.60% per annum amid strong employment data and higher‑than‑expected inflation.

Global equity markets also delivered solid results. The US S&P 500 increased by 1.4%, the UK’s FTSE 100 advanced 2.8%, Japan’s Nikkei surged 5.9%, and Hong Kong’s Hang Seng rose 6.9%.

Chart: Global Investment Market Returns - January 2026

Late‑January market sentiment was dominated by Australia’s latest inflation figures, which confirmed that price pressures remain more persistent than anticipated. Headline CPI rose 3.8% over the year to December, while underlying (trimmed mean) inflation increased to 3.3%, keeping inflation clearly above the RBA’s 2–3% target range. Housing‑related expenses—particularly rents and electricity—continue to drive inflation, signalling that price pressures remain sticky rather than cooling rapidly.

This has pushed interest rate expectations in a more hawkish direction. Markets and major banks now see a meaningful chance of an RBA rate hike in the near term, with attention centred on the upcoming RBA board meeting. Even if rates are left unchanged, the bar for future cuts has risen considerably, and policy is likely to remain restrictive until there is stronger evidence that underlying inflation is truly moving back toward target.

Globally, conditions remain mixed but cautious. After multiple cuts late last year, the US Federal Reserve has paused its easing cycle, citing ongoing inflation risks and resilient economic activity. Central banks in Europe and the UK have also slowed their rate‑cutting pace and continue to emphasise that future decisions will depend on incoming data rather than follow a pre‑set path.

Overall, the message for investors is that interest rates are likely to remain elevated for longer than markets expected just months ago. While a global easing cycle is still anticipated, recent inflation outcomes—particularly in Australia—suggest policymakers will proceed carefully, prioritising inflation control over short‑term growth as 2026 unfolds.

If you have any questions, please contact us.

Disclaimer:

This article is general information only and is not intended to be a recommendation. We strongly recommend you seek advice from your financial adviser as to whether this information is appropriate to your needs, financial situation, and investment objectives.