December 2025 Market Wrap

The Australian share market posted gains in December, with the S&P/ASX 200 Index rising 1.2% to close at 8,714.3 points. The Australian dollar appreciated by 2.0%, currently trading at 66.8 US cents per AUD. The Reserve Bank of Australia (RBA) maintained the Cash Rate at 3.60%, with the next board meeting scheduled for February.

Global equity performance was varied over the month: the US S&P 500 declined by 0.1%, London's FTSE advanced 2.2%, Japan's Nikkei gained 0.2%, and Hong Kong's Hang Seng retreated by 0.9%.

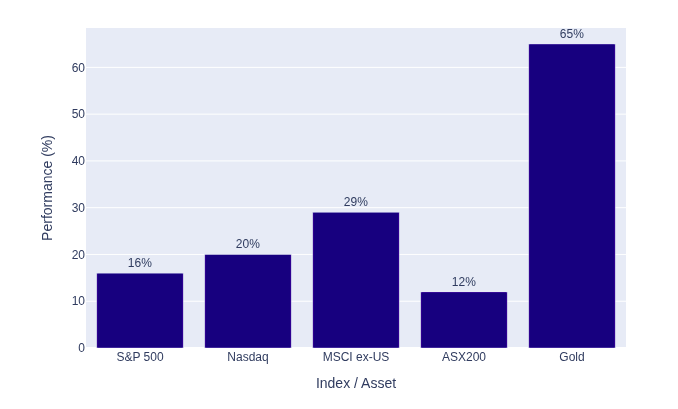

December concluded an impressive year for global markets. Despite earlier geopolitical tensions and uncertainty regarding tariffs, equities ended the year strongly. The US S&P 500 returned approximately 16% for 2025, while the Nasdaq rose more than 20%, fuelled by sustained interest in artificial intelligence and solid corporate earnings.

Chart: Global Investment Market Returns - 2025 Calendar Year

Global Investment Market Performance in 2025

Non-US markets outperformed, with the MSCI ACWI ex-US index increasing nearly 29%, its strongest performance since 2009. Asia demonstrated significant strength—South Korea’s KOSPI surged 76%, and Japan’s Nikkei climbed 28%, reflecting robust semiconductor demand and substantial AI-related investment flows. In contrast, Australia's S&P/ASX 200 returned a comparatively modest 12% for the calendar year.

Commodities performed exceptionally well during 2025. Gold reached record highs, appreciating around 65% over the year, while silver increased by an extraordinary 146%, supported by heightened industrial demand and investor preference for safe-haven assets amid global uncertainty.

Looking ahead to the New Year, global central banks are expected to continue easing monetary policy in 2026, which may support equity valuations and foster corporate investment. Nonetheless, inflation remains a key concern; persistent price pressures could postpone rate reductions—particularly in Australia—and contribute to market volatility.

Investment flows will likely be influenced by technology and energy transition themes. Continued growth is anticipated in artificial intelligence, semiconductor production, and automation, while the worldwide shift towards renewable energy is expected to sustain demand for critical minerals such as copper and lithium—benefiting both commodity prices and related equities.

Geopolitical instability and currency fluctuations will remain significant factors. Ongoing trade disputes and regional conflicts may disrupt supply chains and impact commodity prices, while divergent monetary policies could prompt substantial currency movements.

As always, diversification across asset classes will be essential to manage risk and mitigate market volatility.

For further enquiries, please contact us on 1300 856 338.

This article is general information only and is not intended to be a recommendation. We strongly recommend you seek advice from your financial adviser as to whether this information is appropriate to your needs, financial situation, and investment objectives.