The Australian share market reversed its recent trend in April, with the S&P/ASX 200 Index gaining by 3.6% to close the month at 8,053.7 points. The Australian dollar also gained by 2.6% over the month, with 1 Australian Dollar currently buying 64.1 United States cents.

The Reserve Bank of Australia (RBA) board kept the target Cash Rate on hold at 4.10% per annum in its April meeting. Given the continued decline in domestic inflation and uncertain global outlook, it now appears to be just a question of how large the rate cut will be when the RBA board meet this month (with a 0.25% per annum cut “priced-in” to financial markets).

Global share market returns were mixed in April, with the United States S&P500 Index falling by 0.8%, the London FTSE Index falling by 1.0%, the Japan Nikkei 225 Index gaining by 1.2%, and the Hong Kong Hang Seng Index falling by 4.3% for the month.

Despite a domestic Federal election underway, financial markets continue to be driven by shifts in United States’ President Trump's economic policies. Threats like tariff hikes and intentional meddling with the United States Federal Reserve (the equivalent of the RBA) dampen optimism – only for partial policy reversals to restore some of it.

As it stands, investment markets remain in a state of flux. The key question for investors is whether President Trump is going to pursue his tariff plans in full as first announced, or if he will ultimately relent before his tariff plans push the global economy into recession?

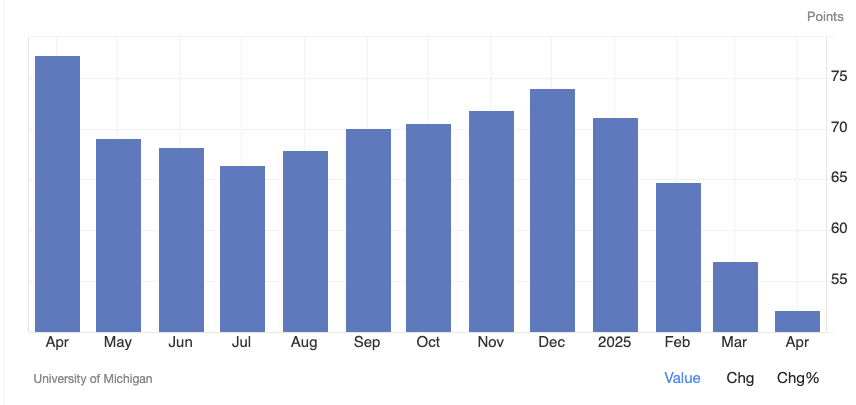

In April, consumer sentiment in the United States fell to the lowest since July 2022 as shown in the chart below.

Source: tradingeconomics.com

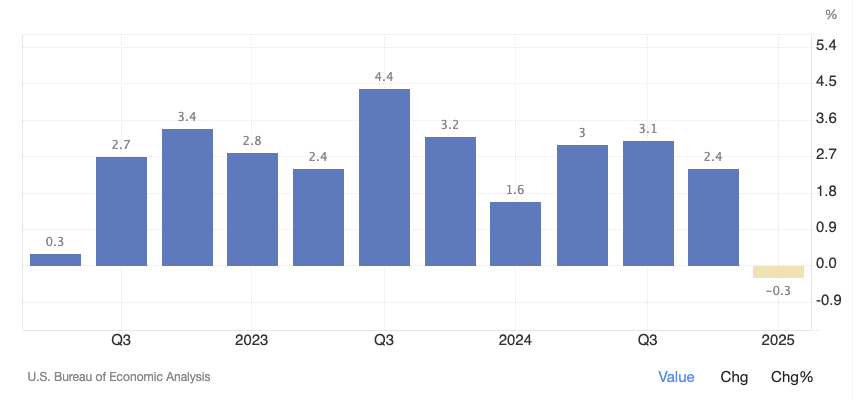

In addition, the United States’ economy contracted at an annualised rate of 0.3% in the first quarter of 2025, marking the first decline since the first quarter of 2022.

Source: tradingeconomics.com

While investment markets have been buoyed in recent times with President Trump suspending many of his most threatened tariffs for 90 days, and with suggestions that he might not increase Chinese tariffs by as much as first thought. It must be said, there is a very real risk that President Trump does not relent (or at least, not fast enough).

If you have questions, please contact us on 1300 856 338.

This article is general information only and is not intended to be a recommendation. We strongly recommend you seek advice from your financial adviser as to whether this information is appropriate to your needs, financial situation, and investment objectives.