The Australian share market experienced a decline in November, with the S&P/ASX 200 Index decreasing by 3.0% to close at 8,614.1 points. The Australian dollar remained stable, trading at 65.5 US cents per AUD. The Reserve Bank of Australia (RBA) maintained the Cash Rate at 3.60%, as elevated inflation levels have diminished prospects for near-term rate cuts.

Global equity performance was mixed during the month: the US S&P 500 advanced by 0.1%, London's FTSE was unchanged, while Japan's Nikkei and Hong Kong's Hang Seng fell by 4.1% and 0.2% respectively.

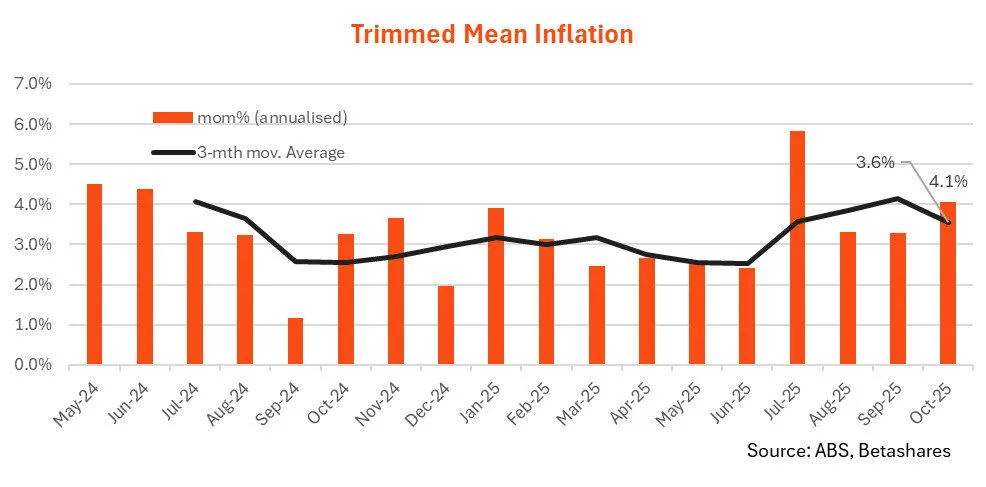

Domestically, October’s Consumer Price Index (CPI) report contributed to volatility in Australian equities and indicated persistent inflationary pressures following the spike observed in the September quarter. The seasonally adjusted trimmed mean CPI increased by 0.33% in October, up from 0.27% in both September and August, driving annual underlying inflation to 3.3%, which exceeds the RBA’s target range of 2–3%.

Although annual inflation metrics are retrospective, monthly trends are critical for monetary policy considerations. Current data suggests an annualised inflation rate of 4.1%, with the three-month average at 3.6%, indicating that price pressures remain substantial.

For the RBA to contemplate rate reductions next year, monthly inflation must reliably fall below an annualised rate of 3%. Until such conditions are met, the possibility of continued higher rates into 2026 persists.

For further enquiries, please contact us on 1300 856 338.

This article is general information only and is not intended to be a recommendation. We strongly recommend you seek advice from your financial adviser as to whether this information is appropriate to your needs, financial situation, and investment objectives.