March 2026 Market Wrap

Ongoing conflict in the Middle East unsettled global investment markets in March, leading to a broad sell‑off across share markets. In Australia, the S&P/ASX 200 Index fell 7.8% to close at 8,481.8 points, marking its largest monthly decline since June 2022.

The Australian dollar weakened by 3.1% over the month to around USD 0.69. At the same time, inflation pressures remained higher than expected, prompting the Reserve Bank of Australia (RBA) to increase the cash rate by a further 0.25% per annum to 4.10% per annum.

Global markets also declined. The US S&P 500 fell 5.1%, the UK FTSE 100 declined 6.7%, Japan’s Nikkei dropped 13.2%, and Hong Kong’s Hang Seng fell 6.9%. Much of this weakness reflected concerns that an escalation of the conflict could push energy prices higher, adding renewed inflationary pressure globally.

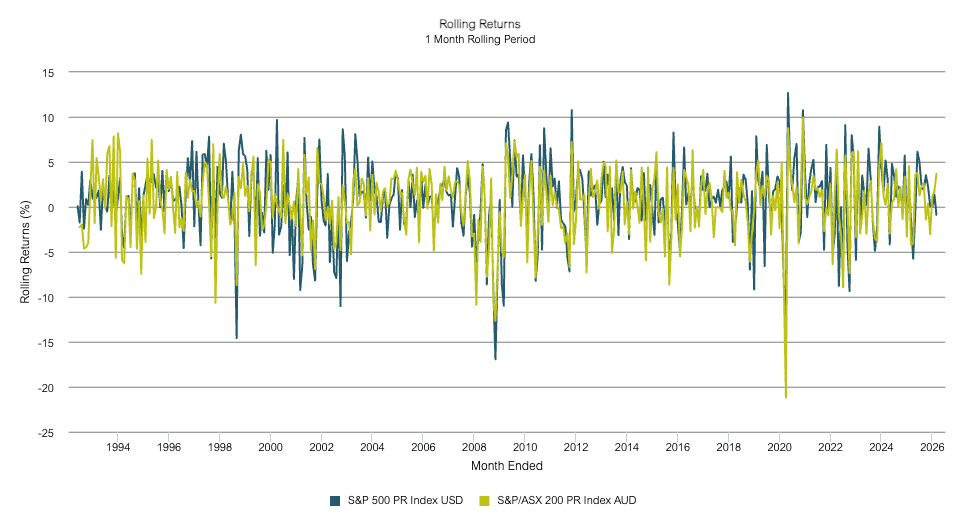

While declines of this magnitude can feel confronting, they are a normal and recurring feature of investing as shown in the chart below.

Source: Lonsec

Historically, share markets experience falls of more than 5% roughly once each year. Even falls of around 10% do not always lead to prolonged downturns, particularly when the economy avoids recession.

Recent history provides useful perspective. In April last year, tariff announcements triggered a rapid 15.8% fall in Australian shares, yet the market recovered fully within weeks. During early 2020, the market fell around 35% in just five weeks before recovering to pre‑crash levels within 13 months.

These periods highlight an important lesson: markets tend to price fear very quickly, while recoveries occur more gradually. Making significant investment decisions based on short‑term emotion has historically produced poorer outcomes than remaining disciplined through volatility. Importantly, not every market correction becomes a prolonged bear market, and when downturns occur without recession, recoveries have typically been faster and more complete.

Looking ahead, markets are weighing the risk that the conflict could be prolonged, keeping fuel and input costs elevated. This could place ongoing pressure on inflation as higher business costs are passed on to consumers, potentially slowing economic growth.

There was some renewed optimism late in the month following comments from President Donald Trump suggesting the conflict may not last “too much longer” and indicating a willingness to leave the fate of the Strait of Hormuz to other nations.

Another encouraging factor is that geopolitical shocks have historically been short‑lived for share markets. The US share market has been higher one year after the onset of conflict around 73% of the time. While oil‑driven shocks can take longer to resolve, history continues to favour patience over panic.

As always, our focus remains on long‑term outcomes rather than short‑term headlines. Portfolios are built with diversification and resilience in mind, recognising that periods of uncertainty are a normal part of investing.

Disclaimer:

This article is general information only and is not intended to be a recommendation. We strongly recommend you seek advice from your financial adviser as to whether this information is appropriate to your needs, financial situation, and investment objectives.