The Australian share market consolidated recent gains, with the S&P/ASX 200 Index gaining by 3.8% in the month of May to close the month at 8,434.7 points. The Australian dollar gained by 0.3% over the month, with 1 Australian Dollar currently buying 64.3 United States cents.

The Reserve Bank of Australia (RBA) board cut the target Cash Rate by 0.25% per annum in its May meeting, with the Cash Rate now at 3.85% per annum. Remarks from the Reserve Bank Governor Michele Bullock indicated that further rate cuts are likely in the near term.

A watering down of United States’ President Trump's tariff plans produced solid returns in global share markets for May. The United States S&P500 Index gained by 6.2%, the London FTSE Index gained by 3.3%, the Japan Nikkei 225 Index gained by 5.3%, and the Hong Kong Hang Seng Index also gained by 5.3% for the month.

The landslide Australian Federal election result in May, with the Labor Government controlling the House of Representatives and the composition of the Senate, means that there is not much standing in the way of the implementation of the extended Division 296 Tax Liability (or so called "$3 million super tax").

This new tax will apply to individual super balances over $3 million, and is an extra 15% tax on top of the existing tax on super earnings, but will now include both realised and unrealised capital gains. A tax on unrealised gains means that you are taxed on an increase in the value of assets even if it is just a paper gain. An asset does not have to be sold for this gain to be taxed.

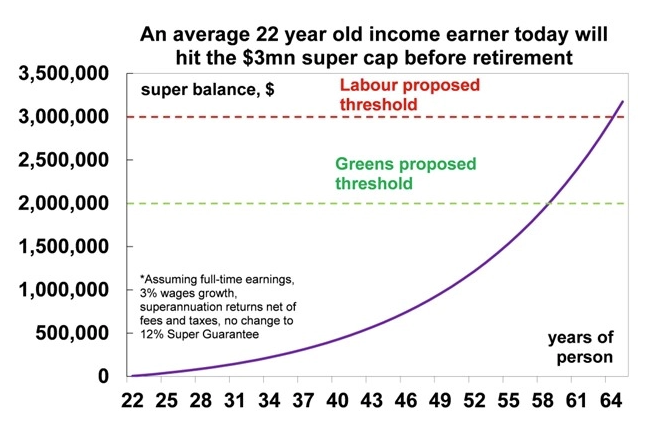

The Government alleges that this new tax only impacts 0.5% of the population or 80,000 people. However, this may be disingenuous as the $3 million threshold is not legislated to be indexed in the future (unlike other super balance thresholds).

Deputy Chief Economist Diana Mousina from AMP has modelled this out to show that the average 22-year-old income earner will hit the cap before they hit retirement unless it is increased in the future.

Source: Morningstar & AMP

Given the Greens support the policy (indeed at a lower threshold of $2 million) it is expected that the new tax will come into effect from 1 July this year.

While the impacts in the short-term may be minimal, those concerned about the impact of this tax in the longer term may wish to consider strategies such as spouse contribution splitting to equalise super balances over time (and potentially avoid and/or reduce the impact of this tax).

If you have questions, please contact us on 1300 856 338.

This article is general information only and is not intended to be a recommendation. We strongly recommend you seek advice from your financial adviser as to whether this information is appropriate to your needs, financial situation, and investment objectives.