May 2026 Market Wrap

Investment markets continued their recovery in May. The S&P ASX 200 rose 0.8% to close at 8,731 points, while the Australian dollar weakened slightly by 0.3%. The Reserve Bank of Australia also increased interest rates again, taking the cash rate to 4.35% per annum, the highest level in over a decade and continuing to pressure borrowing capacity.

Global markets delivered solid but uneven returns. The US market (S&P 500) gained 5.1%, while Japan surged 11.9%. The UK rose a modest 0.3%, and Hong Kong declined by 2.2%. The resilience in US markets follows a strong April, reflecting improved investor sentiment as geopolitical concerns eased.

The key development during the month was the 2026/27 Federal Budget, which includes some of the most significant proposed changes to investment taxation in recent years. In principle, a Federal Budget should focus on balancing the nation’s finances, meaning consideration should be given not only to how revenue is raised, but also how it is spent.

Source: Parliamentary Budget Office

While the Government is targeting meaningful savings within the National Disability Insurance Scheme (NDIS), much of the public focus has been on the proposed tax changes.

From 1 July 2027, the Government has proposed replacing the 50% capital gains tax discount with an indexation approach, alongside the introduction of a minimum 30% tax on capital gains. Negative gearing would also be restricted to newly built residential properties. A further measure includes a 30% minimum tax on discretionary trusts from 1 July 2028, with limited flexibility to restructure existing arrangements.

These changes represent a clear shift away from traditional investor tax concessions. While the stated objective is to redirect capital towards housing supply and broader economic priorities, there remains limited focus on addressing key structural constraints such as infrastructure, planning delays and labour shortages, all of which are critical to improving housing supply.

A key implication is that the proposed 30% minimum tax on capital gains would apply broadly to investments held outside superannuation, including shares and other growth assets. While superannuation remains largely unchanged and new residential property receives targeted support, many other investments may face structurally higher tax outcomes. This further skews incentives towards holding wealth in the family home or within superannuation, rather than across diversified asset classes and structures.

Importantly, these proposed changes are widely expected to place downward pressure on residential property prices in the short term. This sits at odds with the Government’s continued support for first home buyers, including the expansion of the 5% deposit guarantee scheme, which encourages market entry with minimal equity and has proven popular.

This policy tension creates a challenging dynamic. On one hand, new entrants are being encouraged to purchase property with low deposits, while on the other, policy settings may contribute to softer house prices. In practice, this could expose newer buyers to short‑term value declines and potentially widen the generational wealth divide, rather than narrow it.

There is also ongoing debate as to whether the housing measures will achieve their intended outcomes. While reducing tax incentives may dampen demand for established properties, it may also discourage investment in housing, noting that private investors fund a significant portion of rental supply at a time when Australia already faces a structural housing shortage.

More broadly, these changes reinforce the continuing shift in policy settings and highlight the importance of careful investment structuring in a more complex and less concession‑driven environment.

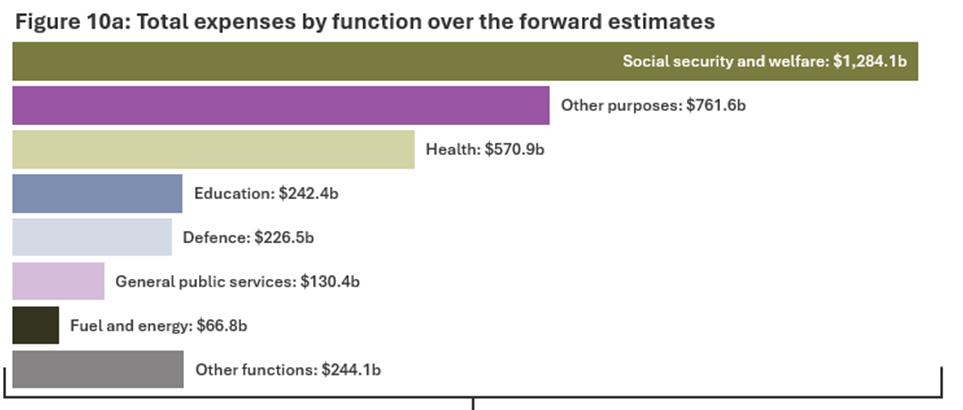

Finally, there is increasing scrutiny on the broader fairness of the system. The family home remains fully exempt from the Age Pension means test, despite the Age Pension costing approximately $62.2 billion per year, around 8.4% of total government expenditure, and more than the NDIS, which has been a key focus in the Federal Budget.

At the same time, Age Pension renters are only permitted an additional $242,000 in assessable assets compared to homeowners before their entitlements begin to reduce. This disparity continues to encourage wealth retention in the family home and is likely to remain a key area of policy debate into the future.

This article contains general information only and does not constitute financial advice. You should consider seeking advice from your financial adviser to determine whether this information is appropriate for your personal circumstances, financial situation and investment objectives.